1. Introduction: From Banyan Trees to High-Frequency Trading

The history of Indian commerce is a study in dramatic contrasts. In 1875, the Bombay Stock Exchange (BSE) began with just 22 brokers gathering under a banyan tree, each investing a single rupee. Today, the National Stock Exchange (NSE) is a technological titan, a $5.3 trillion market capable of processing 160,000 orders per second.

Yet, while India’s financial securities have achieved world-class unification and seamless digital execution, its agricultural sector remains a different world entirely. While a trader in Mumbai can buy shares in a company based in Assam in milliseconds, the journey of a bag of grain is still caught in a “fragmented mosaic” of local regulations. Why has the financial sector achieved light-speed integration while agricultural markets remain a collection of thousands of localized entities? To understand the future of the Indian economy, we must dissect the digital and structural evolution currently reshaping the “Digital Harvest.”

2. Takeaway 1: India is Not One Market, But Thousands of “Silos”

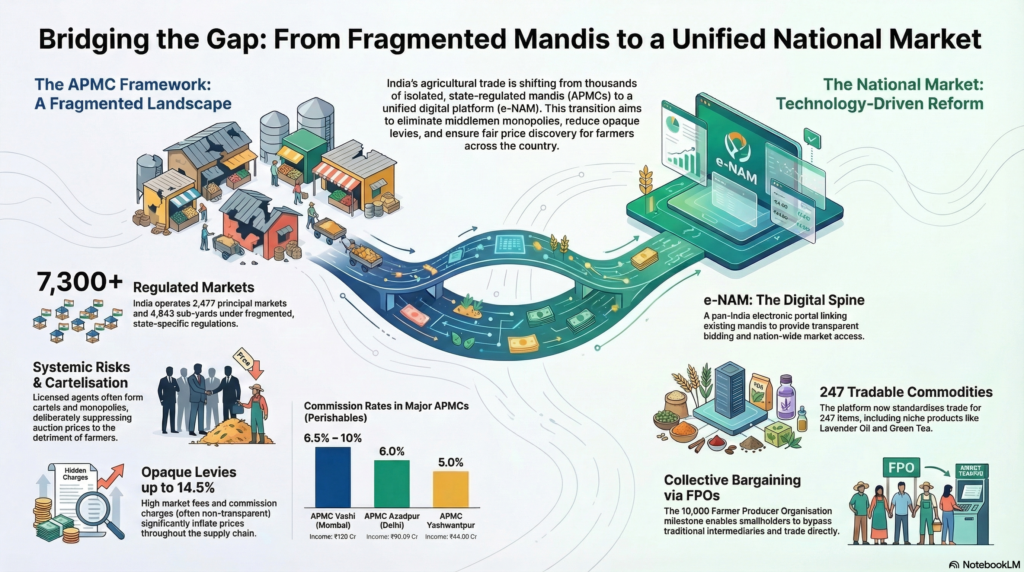

The primary hurdle to a unified Indian economy isn’t technology, but geography-based regulation. Despite being one nation, India is economically divided into a mosaic of approximately 7,320 distinct entities. Under the Agricultural Produce Market Committee (APMC) Act, states are geographically partitioned into market areas where the law mandates that the “first sale” of notified agricultural commodities can only occur under specific local aegis.

This system is divided into two distinct tiers: 2,477 principal regulated markets and 4,843 sub-market yards. Because each area is administered by a separate APMC with its own marketing regulations and fees, the reality is that India has “not one, not 29, but thousands of agricultural markets.” This fragmentation creates significant silos, preventing the formation of a truly common national market.

3. Takeaway 2: The “Hidden” Mandi Tax and the Cost of a Tomato

Moving produce through these silos comes with a significant price tag in the form of multiple, non-transparent fees. These include mandi taxes, licensing fees for agents, and various cesses that create a cascading effect on the final price paid by consumers.

Data from the Economic Survey highlights the stark regional disparities in these levies:

- Rice/Paddy: Procurement charges reach as high as 19.5% of the Minimum Support Price (MSP) in Andhra Pradesh and 14.5% in Punjab.

- Wheat: Statutory levies and taxes hit 14.5% in Punjab and 11.5% in Haryana.

As a journalist, the most striking detail is how these operations act as a source of political power. While market fees are collected like a tax, the revenue frequently bypasses the State exchequer, meaning it does not require legislative approval for utilization. Furthermore, because the number of licenses granted is kept small, it creates a “premium” for the right to trade—a premium that is widely believed to be paid in cash, hidden from any official scrutiny.

“The rate of commission charged by the licensed commission agents is exorbitant, because… the commission is charged on the entire value of the produce sold.”

4. Takeaway 3: The Regulator-Trader Conflict of Interest

A fundamental structural flaw within the APMC system is a glaring conflict of interest. The committees are designed to be regulators, yet the members and chairmen are often elected or nominated from the very group of commission agents and traders they are tasked with overseeing. This leads to “cartelization,” where agents coordinate to restrain from higher bidding during auctions, procuring produce at manipulatively low prices before sharing the “spoils.”

The Spoils of the Mandi:

- Monopoly Power: Licensed agents wield total control within their notified area, creating high entry barriers for competitors.

- Entry Barriers: Prohibitive license fees and high rents for market stalls ensure that only the village or urban elite can operate.

- Payment Withholding: Agents frequently block parts of farmer payments for fictitious reasons or refuse to provide official payment slips, which are necessary for farmers to access institutional loans.

5. Takeaway 4: The e-NAM Paradox—Expanding Tools, Shrinking Trade?

The National Agriculture Market (e-NAM) was launched to solve these issues by linking mandis into a unified electronic portal. By late 2025, the platform achieved a milestone by expanding its tradable items to 247 commodities, including high-value niche products like Lavender Oil, Green Tea, and Virgin Olive Oil.

However, as an agri-tech consultant, I find the emerging “e-NAM Paradox” concerning. Despite having over 1,656 mandis integrated and 1.80 crore farmers registered, the actual volume of cross-border trade is struggling. Reports from Q1 FY26 indicated a staggering 62% decline in inter-state trade on e-NAM.

This suggests that the transition to the e-NAM 2.0 upgrade is facing a significant hurdle. Digital tools alone cannot bridge the gap; the “missing links” remain standardized quality assaying and physical logistics. Without absolute trust in the quality of goods being bid on from a thousand miles away, the digital marketplace remains limited by physical boundaries.

6. Takeaway 5: The 2025 “Agri-Pause”—A New Deal for Rural Labor

In a landmark shift for rural development, the Viksit Bharat-G RAM G Act of 2025 has replaced previous employment schemes like MGNREGA. This transition represents a strategic move toward the “Viksit Bharat National Rural Infrastructure Stack,” focusing on “durable assets” rather than temporary work.

A key innovation of the Act is the “60-day agricultural pause.” This mandates a halt in public works during the peak sowing and harvesting seasons.

Why this is a strategic “win-win”:

- Labor Availability: It prevents government-funded works from competing with farmers for labor, stabilizing rural wages during critical windows.

- Asset Creation: When work resumes, it focuses on building essential infrastructure like cold storage and drying yards.

- Technical Capacity: The Act increases the administrative expenditure ceiling to 9%, allowing for the staffing and technical capacity required to build professional-grade infrastructure.

- Financial Resilience: The Act increases guaranteed workdays to 125 per year and supports credit expansion, such as raising Kisan Credit Card limits from ₹3 lakh to ₹5 lakh.

7. Conclusion: The Convergence of Two Indias

The evolution of India’s markets is currently driven by a “triad of growth”: the e-NAM digital platform, a strengthened credit framework, and the milestone of 10,000 Farmer Producer Organizations (FPOs) achieved in early 2026. While the nation’s stock exchanges have provided a world-class template for transparency, the agricultural sector is only now undergoing its own “financialization” through collectives and digital bidding.

The transition from informal gatherings under banyan trees to a $5 trillion digital economy is complete for the financier. For the farmer, that journey is still in its most volatile phase. As we look toward an integrated future, we must ask: In a nation where we can trade stocks at the speed of light, how much longer should it take for a farmer in Rajasthan to get a fair price from a buyer in Tamil Nadu?