Engineering 1:199 Risk-Reward Asymmetry: Sophisticated Nifty Modeling for the March 2026 Expiry

1. Introduction: The Mathematics of Market Uncertainty

Predicting the exact trajectory of the Nifty Index is often a fool’s errand, characterized by the chaotic noise of short-term volatility. For the retail trader, the market feels like a series of guesses; for the strategist, it is a series of calculations. To navigate the March 2026 expiry, we must move beyond directional bias and embrace “Strategic Derivative Modeling.” By utilizing advanced Opstra configurations, we can shift from speculative “guessing” to precise “projection,” mapping out how volatility expansion/contraction and price movement impact the profitable Delta/Theta envelope of our portfolio.

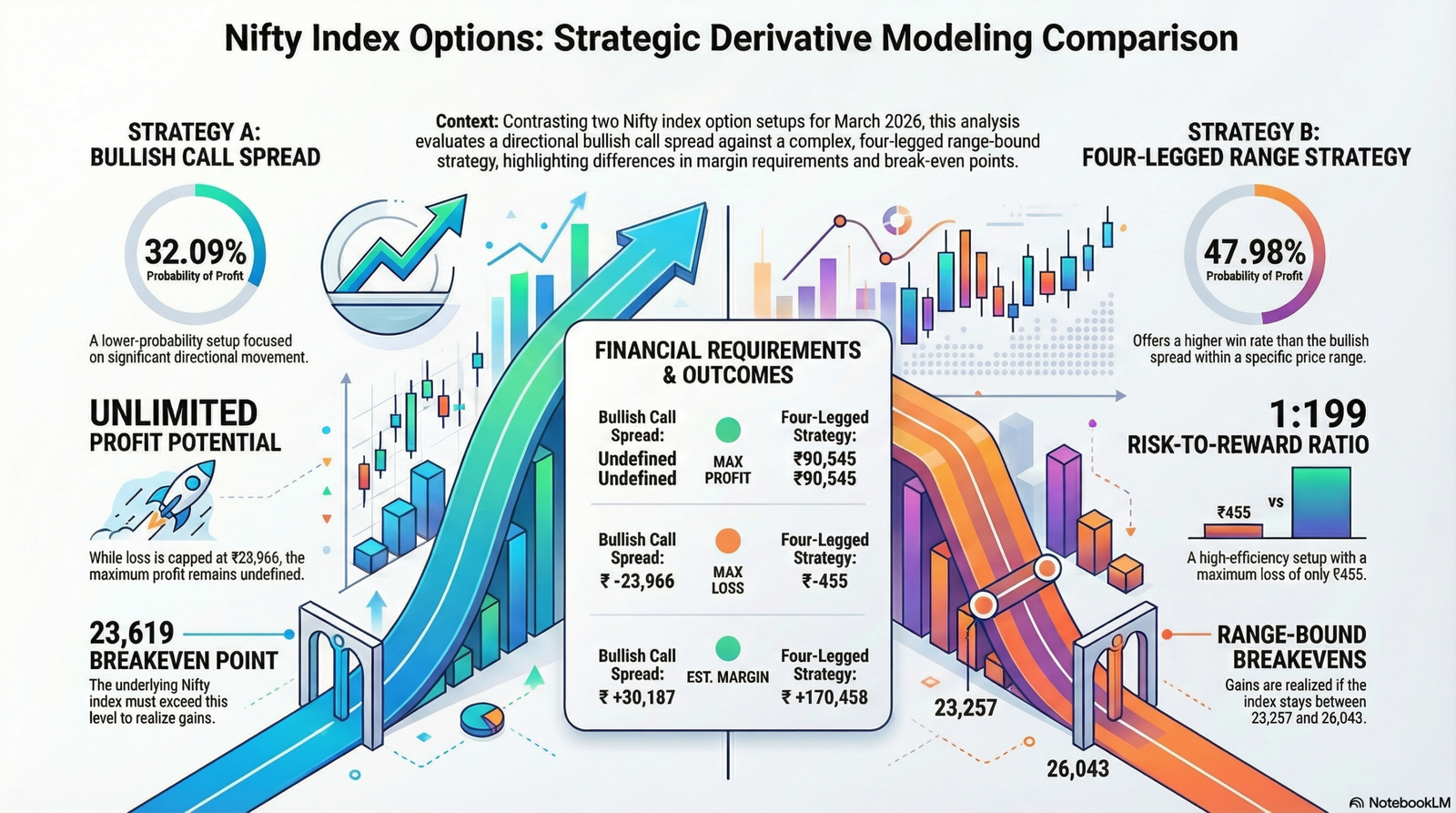

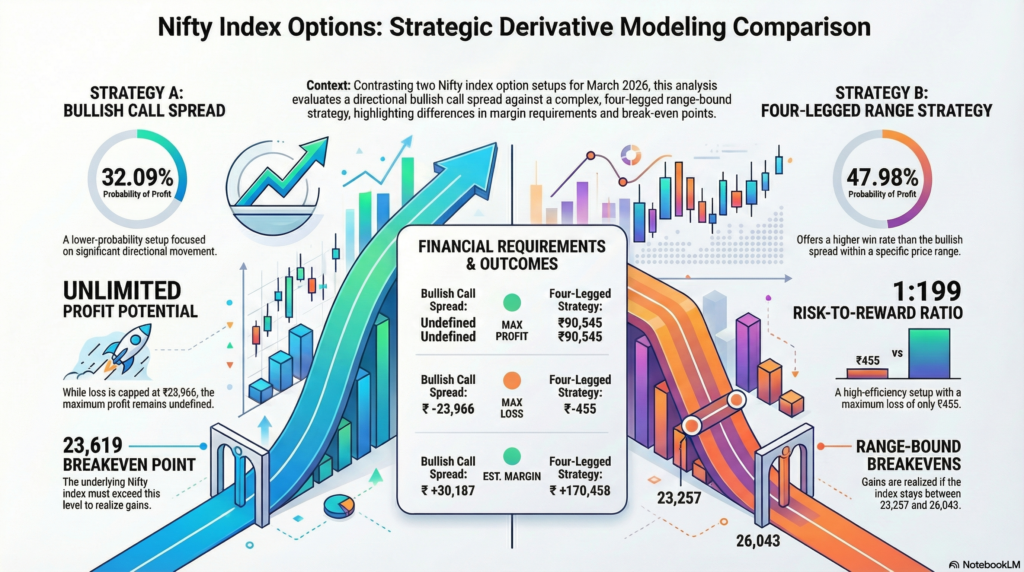

2. The 1:199 Ratio: Redefining “Safe” Risk

Analysis of a complex four-legged strategy—specifically an Iron Butterfly variation—reveals a statistical profile that challenges conventional market wisdom. The data for the March 2026 expiry (per Screenshot 094223) shows a Maximum Loss of a mere ₹ -455. In the context of a professional portfolio, this is essentially “noise”—a loss of just -0.27% of capital. Contrast this with a Maximum Profit of ₹ +90,545, and we arrive at a staggering 1:199 risk-to-reward ratio.

This asymmetry is achieved through a significant net credit received against a meticulously capped risk floor. It allows a trader to maintain a high-conviction stance with a risk profile lower than a single stop-loss hit in a standard futures contract.

“By comparing these configurations, a trader can assess the risk-to-reward ratios and volatility exposure.”

3. The Trap of “Unlimited” Potential

Retail participants are frequently seduced by “undefined” upside, often opting for structures like the 1:2 Call Backspread (Screenshot 094004). While this setup—selling a 23050CE and buying two 23250CEs—is a classic bullish proxy with no ceiling on gains, it contains a significant statistical trap when compared to the engineered Iron Butterfly:

- 1:2 Call Backspread: While profit is “Undefined,” the Probability of Profit (PoP) is a meager 32.09%. More critically, the Max Loss is a devastating ₹ -23,966 (-79.39% of margin).

- Iron Butterfly Variation: This strategy caps the upside at ₹ 90,545 but elevates the PoP to 47.98% while slashing the Max Loss to nearly zero (₹ -455).

The “unlimited” allure of the backspread effectively asks the trader to accept 50 times the risk of the complex strategy for a significantly lower statistical chance of success. In quantitative terms, the Iron Butterfly offers far superior Capital Allocation Efficiency.

4. The “Tent” of Probability: Precision Over Direction

The payoff graphs (Screenshots 094257 and 094316) illustrate the “tent” structure of this trade. Unlike a backspread that requires an aggressive Gamma move to reach profitability, the Iron Butterfly is designed to capture value within a specific range. The peak of this “tent”—where maximum profit is realized—sits precisely at the 24650 short strike.

The strategic advantage lies in the breakeven range of 23257.0 to 26043.0. By examining the standard deviation lines on the Opstra model, we can see that this nearly 2,800-point window encompasses almost the entire +/- 1 Standard Deviation (1σ) move. This provides a massive “margin for error,” allowing the trade to remain viable even amidst significant market swings, provided the index stays within this statistically probable zone.

5. The Capital Premium: Why Certainty Costs More

In the derivatives market, certainty is a premium asset. There is a clear trade-off between the entry cost and the risk-mitigation profile:

- 1:2 Call Backspread Margin: ₹ 30,187

- Iron Butterfly Margin: ₹ 170,458

While the Iron Butterfly requires higher collateral, the “entry fee” buys a drastically superior Return on Capital (ROC). At the peak profit level, the Iron Butterfly delivers an ROC of 53.12%, compared to the backspread which would require a massive, outlier move in the Nifty just to break even. High margin requirements in this context are not a barrier, but a purchase of “engineered certainty” and a protected downside.

“The sources serve as a financial modeling tool to help investors project outcomes for advanced derivative portfolios.”

6. Conclusion: From Prediction to Projection

Successful trading as we approach 2026 is not predicated on being “right” about market direction, but on being “right” about the internal structure of the trade. The transition from a 1:2 Call Backspread to a multi-legged Iron Butterfly represents a move from gambling on outliers to harvesting probability.

As you evaluate your strategy for the coming years, ask yourself: would you prefer the “lottery ticket” of unlimited upside paired with a high-risk floor, or the “engineered certainty” of a high-probability model that covers a full standard deviation of market movement?