In the quiet corners of almost every Indian home lies a staggering paradox. It is found in a grandmother’s bangles locked away for decades, the intricate necklaces gifted as “family insurance” at weddings, and the coins ritualistically purchased during the auspicious hours of Akshaya Tritiya. In India, gold is rarely a mere commodity; it is memory, security, and a symbol of status woven into the cultural fabric.

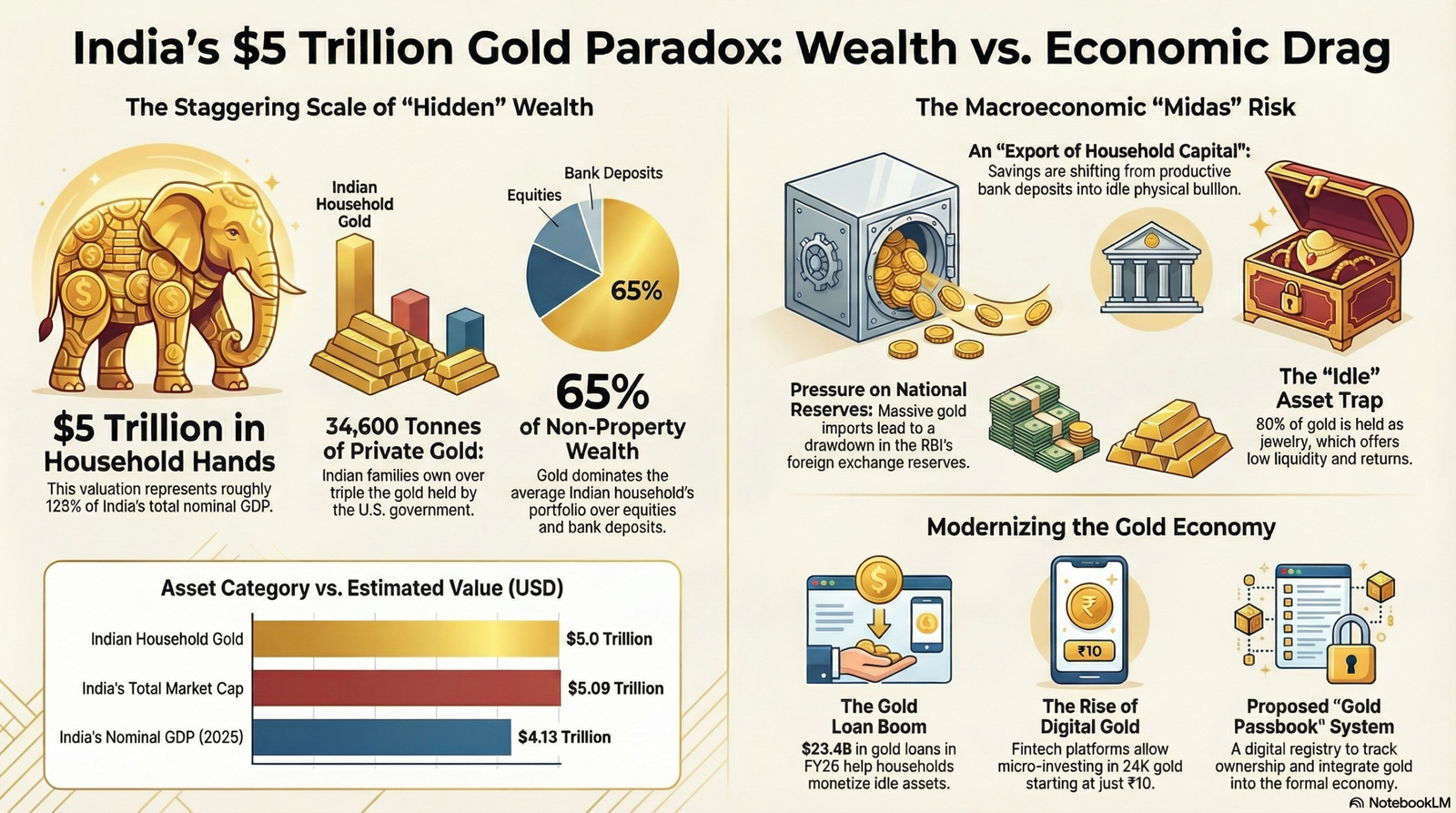

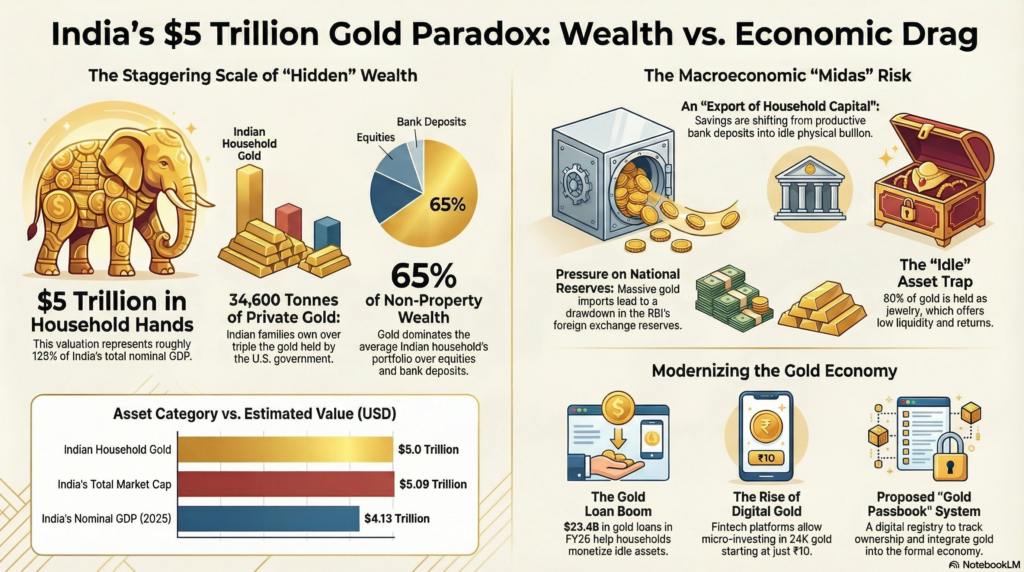

But when these individual stories are aggregated, the scale transitions from personal sentiment to a gargantuan macroeconomic weight. Indian households currently sit on a gold pile estimated at 28,000 to 34,600 tonnes. Following a relentless rally in global prices, this hoard is now valued at approximately $5 trillion. While this “golden touch” reflects immense private wealth, it presents a “Midas” dilemma: like the mythical king, India has turned its savings into an asset that is glittering, precious, and—economically speaking—largely frozen. This article explores why this hoard is simultaneously India’s greatest safety net and its most significant drag on capital productivity.

The Wealth That Doesn’t Work: A Stock vs. Flow Paradox

For the first time in modern history, the value of gold held by Indian citizens has effectively overtaken the size of the nation’s entire annual economic output. Recent estimates suggest that the $5 trillion household gold hoard now exceeds India’s nominal GDP, projected at approximately $4.125 trillion for the 2025-26 financial year.

To understand the irony of being “wealthy but capital-starved,” one must look at the “Stock vs. Flow” distinction. GDP represents a “flow”—the value of goods and services produced in a single year. Household gold represents a “stock”—wealth meticulously accumulated over generations. Today, this stock represents a staggering 65% of all non-property household wealth in India. Its valuation now rivals the nation’s total stock market capitalization (~$5.09 trillion), yet while the stock market fuels corporate growth, gold sits idle in cupboards, yielding zero productivity for the broader economy.

The “Midas Effect”: Exporting India’s Household Capital

While owning $5 trillion in gold sounds like a position of strength, analysts at Kotak Institutional Equities warn of a structural “Midas effect” that drains the domestic financial system. Every gram of gold purchased is effectively a “conversion of financial savings into physical assets,” which Kotak characterizes as an “export of household capital.”

The scale of this leakage is profound. Since 2011, India has spent an estimated $500 billion on gold imports—more than double the $200 billion in net Foreign Portfolio Investment (FPI) flows into Indian debt and equity during the same period. This preference for bullion over bank deposits puts immense pressure on the Reserve Bank of India’s (RBI) foreign exchange reserves and widens the current account deficit (CAD).

“This dynamic can lead to a drawdown in the Reserve Bank of India’s foreign exchange reserves… limiting reserve money creation and tightening system liquidity, potentially weighing on deposit growth.” — Kotak Institutional Equities

In a global context, this gold fever is a logical, albeit expensive, hedge. As geopolitical tensions like the Israel-Iran conflict escalate and nations react to the “weaponization of the dollar,” Indian households and the RBI (which added 75 tonnes to its reserves since 2024) are seeking strategic autonomy. However, this flight to safety comes at the cost of the domestic liquidity needed to fund India’s infrastructure and industrial ambitions.

The Jewelry Paradox: Why $5 Trillion Feels Like Zero

Standard economic theory suggests a “wealth effect”—as asset prices rise, owners spend more. Yet, despite gold prices surging 65% in 2025 alone, there has been no corresponding boom in Indian consumer spending.

The reason lies in the “Jewelry Paradox.” Approximately 75–80% of household gold is held as ornaments, not as marked-to-market investment bars. Jewelry carries deep emotional weight and is rarely viewed as an asset to be liquidated for a profit. Furthermore, once you factor in high “making charges” and storage risks, the barriers to selling are high. As BlackRock CEO Larry Fink recently noted, gold is “independent of India”—it grows with global fears and currency debasement, but it doesn’t grow with the Indian economy. When capital is locked in a necklace, it is capital taken out of the productive cycle.

The Rise of the “Shadow Bank”: Gold Loans as Secured Strategy

If Indians are unwilling to sell their gold, they are increasingly desperate to leverage it. We are witnessing a massive shift in the banking sector, where gold is being transformed into a “shadow financial system.”

In FY25 and FY26, banks and NBFCs extended an estimated $20 billion to $23.4 billion in gold loans—a massive jump from the $3 billion annual average seen between FY22 and FY24. This isn’t just a win for consumers; it’s a strategic pivot for lenders. Facing risks in other retail sectors, Indian banks are increasingly favoring “secured retail credit.” By using gold as collateral, lenders can mitigate risk while providing “working capital” to low-income households for healthcare, education, or small businesses. This acts as a vital, if imperfect, bridge between a non-productive asset and productive economic use.

The Radical Proposal: A National Gold Passbook

To solve the $5 trillion dilemma, some strategists have proposed the “Hidden Gold” framework: a National Gold Passbook System linked to Aadhaar and PAN. This would essentially treat gold like a bank deposit, bringing the informal hoard into the light of digital governance.

According to the “Hidden Gold” proposal, a blockchain-based system could offer transformative benefits:

- A Trillion-Rupee GDP Boost: Integrating unaccounted gold could increase India’s GDP figures by 10–20% (an estimated ₹7–14 lakh crore increase).

- Monetary Expansion: The system could create a ₹3–5 lakh crore new monetary base, allowing the RBI to issue currency backed by documented gold certificates.

- Transparency & Safety: Traceability would lead to a 30–40% decrease in black money transactions and an 80–90% reduction in gold-related theft and fraud, as stolen gold would be unsellable in a registered system.

- Real-Time Utility: Utilizing blockchain would allow gold to be used as a liquid currency for real-time encashment and trade via QR codes.

The challenges are admittedly steep, requiring a “demonetization-level” effort to overcome cultural resistance to asset declaration and privacy concerns.

Conclusion: Redefining the “Golden Bird”

India was once historically celebrated as the Sone ki Chidiya (the Golden Bird). Today, with $5 trillion in private reserves, that title is more accurate than ever. Yet, the nation faces a modern crisis of choice. While this gold provides an unparalleled safety net for millions of families against global uncertainty and dollar volatility, its status as an “idle” asset outside the formal system represents a massive opportunity cost.

The transition from viewing gold as “static security” to “productive capital” is beginning to take shape through the explosion of gold-backed lending and digital instruments. As the global order shifts and strategic autonomy becomes paramount, India must decide: In an era of digital transparency and rapid growth, can we afford to keep $5 trillion of our nation’s wealth locked in a cupboard?