HDFC Bank’s $12 Billion Disappearance: A Learner’s Guide to Market Reactions

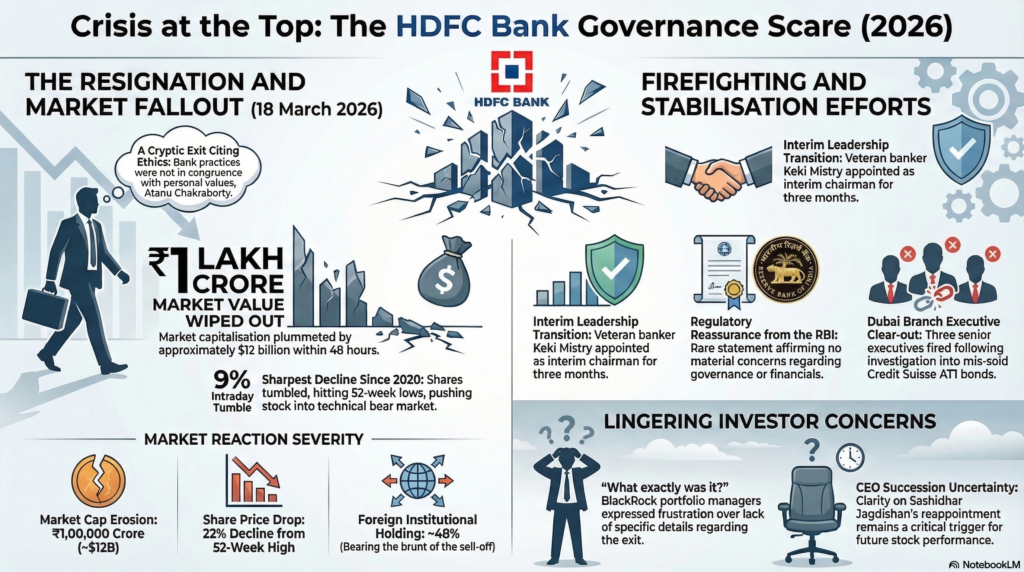

In the sophisticated world of high-stakes finance, a bank’s most vital asset is not the liquidity in its vaults, but the perceived integrity of its leadership. On March 18, 2026, that integrity was called into question when Atanu Chakraborty, the part-time Chairman of HDFC Bank, abruptly resigned. The resulting shockwave erased approximately $12 billion in market value in a single day.

For the aspiring financial professional, this case is a masterclass in how “governance risk” can supersede fundamental financial strength.

——————————————————————————–

1. The Catalyst: A Resignation That Rocked the Market

The crisis was ignited by a resignation letter characterized by its “cryptic” and damaging brevity. Atanu Chakraborty, a 1985-batch IAS officer and former Secretary of Economic Affairs, stepped down citing a fundamental clash between the bank’s internal culture and his personal principles. He specifically highlighted that “happenings and practices” he observed over the last two years were “not in congruence with [his] personal values and ethics.”

When pressed by the board to elaborate, Chakraborty refused to provide specific instances or name individual actors. This refusal created a vacuum of information that the market immediately filled with worst-case scenarios.

| Official Bank Stance | The Chairman’s Stated Reason |

| The board expressed “bafflement,” claiming they were unaware of any material issues or regulatory red flags that would justify such a move. | Cited a direct conflict with “personal values and ethics” regarding bank practices observed over the previous 24 months. |

| Management and every board member tried to persuade him to stay or “take back some of the language” in the letter to prevent market panic. | Refused to soften the language or relent, signaling a complete breakdown in the relationship between oversight and executive management. |

While the bank attempted to frame the exit as a personal matter, the market viewed the “ethics” terminology as a red alert regarding the bank’s internal health.

——————————————————————————–

2. Visualizing the Damage: The Numbers Behind the Crash

In finance, ambiguity is a sell signal. Because HDFC Bank is a cornerstone of the Indian equity market, the reaction was swift and unforgiving.

- Market Cap Erosion: The bank’s total valuation plummeted by approximately ₹1 lakh crore (~$12 billion) almost instantly.

- Share Price Percentage Drop: The stock experienced a peak intraday plunge of 8.7% to 9%, its most severe contraction since the 2020 global pandemic crash.

- Technical Milestone: The stock hit a 52-week low of ₹772 on the BSE—a staggering fall from its peak of ₹1,020 recorded just months prior in October 2025. This 24% decline officially placed the stock in a “technical bear market.”

The “So What?” for the Learner Why does a 9% drop in HDFC Bank matter more than a 20% drop in a mid-sized firm? HDFC is classified as a “Systemically Important Bank.” Its sheer scale means it is “too big to fail” without threatening the stability of the entire national economy. When a heavyweight of this magnitude enters a technical bear market, it creates an “index drag,” pulling down the Nifty 50 and Sensex regardless of how well other companies are performing.

While the numbers were devastating, the true cause of the sell-off lay in the psychological shift among the bank’s largest supporters.

——————————————————————————–

3. The Investor Perspective: Why “Cryptic” is Dangerous

Institutional giants like BlackRock and Macquarie, who manage trillions globally, prioritize predictability over almost any other metric. During a heated emergency call, Prashant Periwal, a portfolio manager at BlackRock, demanded transparency: “What exactly was it? Because he was the chairman of the bank. He was not like any other employee.”

The market’s panic stems from three primary governance fears:

- Ambiguity vs. Certainty: Investors can price in “bad news” (like a fine or a missed earnings target). They cannot price in a “mystery.” Ambiguity suggests a “ticking time bomb” that may explode only after further investigation.

- Governance Overhang: The mention of “ethics” created a “Governance Overhang.” This was exacerbated by the looming reappointment of CEO Sashidhar Jagdishan. Investors feared the Chairman’s exit was a “no-confidence” vote against the CEO’s leadership and his upcoming term extension.

- FII Influence: Foreign Institutional Investors (FIIs) hold nearly 48% of HDFC Bank. Global funds are extremely sensitive to “governance optics.” When they detect a stalemate between the Board and Management, they de-risk by selling first and waiting for clarity later.

As investors scrambled for answers, several months of mounting regulatory friction began to surface, revealing the “happenings” Chakraborty likely alluded to.

——————————————————————————–

4. Peeling Back the Layers: Tensions and Operational Scandals

From a governance perspective, the “values and ethics” mentioned were not abstract. They were tied to a series of disciplinary actions and regulatory failures that suggested a culture of “growth at any cost.”

| Friction Point | Context/Outcome |

| AT1 Bond Mis-selling | The bank fired three senior executives—Sampath Kumar (Group Head of Branch Banking), Harsh Gupta, and Payal Mandhyan—after high-risk “Additional Tier 1” bonds were mis-sold to Non-Resident Indians (NRIs) as safe “fixed-maturity” instruments. |

| Dubai Operations Ban | In September 2025, the Dubai Financial Services Authority (DFSA) banned HDFC Bank from onboarding new clients at its Dubai International Financial Centre (DIFC) branch due to severe compliance and advice failures. |

| CEO Performance Review | Chakraborty reportedly insisted on a rigorous, independent performance review before approving a third term for CEO Sashidhar Jagdishan, leading to a “personal relationship issue” within the boardroom. |

| Post-Merger Integration | Following the $10 billion merger with HDFC Ltd, the bank faced significant internal friction regarding cultural alignment and the speed of realizing merger synergies. |

The “So What?” for the Learner Ethics in banking are not just moral guidelines; they are operational requirements. The mis-selling of Credit Suisse-linked AT1 bonds to retail customers and the regulatory ban in Dubai were tangible evidence of a breakdown in oversight. For a Chairman with a background in administrative discipline, these events represented systemic failures that management appeared to be downplaying.

Recognizing the threat of a wider financial contagion, the regulatory and governmental machinery moved into “firefighting mode.”

——————————————————————————–

5. The Firefighting Phase: Stabilization and Recovery Efforts

To prevent a crisis of confidence from turning into a run on the bank, a coordinated stabilization effort was launched:

- The Interim Anchor (Keki Mistry): The bank appointed 71-year-old group veteran Keki Mistry as Interim Chairman for three months. His appointment, approved immediately by the RBI, was designed to signal “steady hands” and institutional continuity.

- The Regulator’s Reassurance (RBI): The Reserve Bank of India issued a rare, definitive statement affirming they had “no material concerns” regarding the bank’s governance or financials, effectively acting as a psychological floor for the stock price.

- Government Endorsement: M. Nagaraju, the Financial Services Secretary, publicly stated that the bank possessed “strong fundamentals,” providing the state’s backing to the bank’s stability.

The bank is currently fast-tracking Nomination and Remuneration Committee (NRC) meetings to finalize the CEO’s future and appoint a permanent successor to Chakraborty.

——————————————————————————–

6. Key Insights: Lessons for the Aspiring Learner

The HDFC Bank crisis serves as a critical case study for any student of corporate governance:

- Insight 1: Governance is Value. A bank’s primary product is trust. If ethical concerns emerge, the resulting “uncertainty premium” will erase market value faster than strong earnings can rebuild it.

- Insight 2: Leadership Continuity is a Market Trigger. High-profile exits post-merger signal internal instability. Markets demand clarity on the “CEO-Chairman” dynamic; any friction here is viewed as a systemic risk.

- Insight 3: The Regulator is the Final Arbiter. In a governance vacuum, the market looks to the Central Bank (RBI) for truth. Without the RBI’s “no material concerns” statement, the HDFC sell-off could have spiraled into a broader systemic crisis.

HDFC Bank remains at a critical juncture. While its balance sheet remains robust, its recovery depends entirely on its ability to prove that its “values and ethics” are as resilient as its profit margins.