Welcome, students. To understand the inner workings of a modern global bank, one must look beyond the balance sheet and into the boardroom. A bank is not merely a vault for capital; it is a delicate ecosystem of authority designed to balance the aggressive pursuit of profit with the absolute necessity of ethical stability. We often speak of “Governance Overhang”—a mental model where the market prices in the risk of leadership friction. When the “Moral Compass” of an institution (the Chairman) and its “Operational Engine” (the CEO) fall out of sync, the “Fuel” (investor capital) evaporates with terrifying speed.

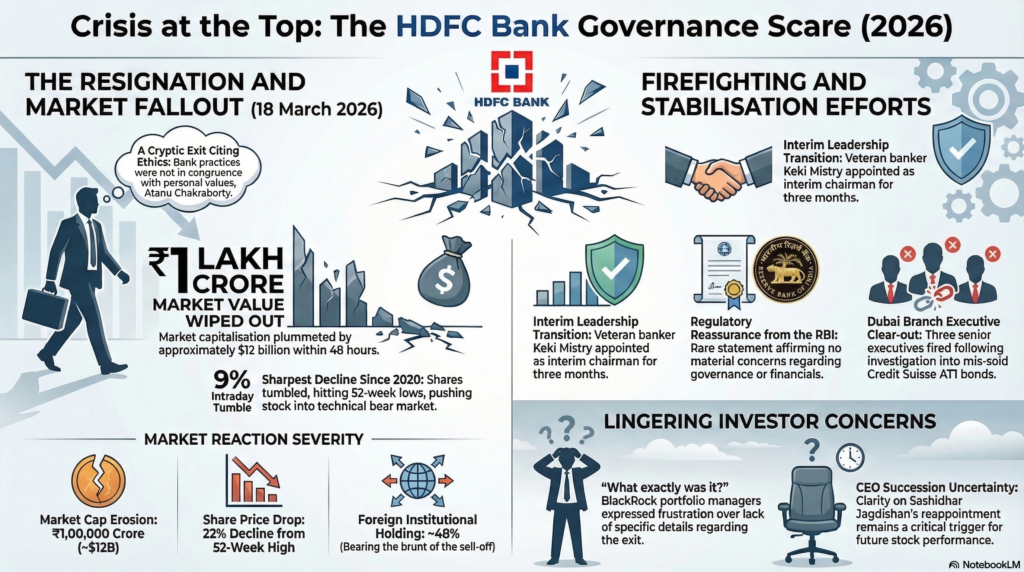

To illustrate this, we will deconstruct the March 2026 leadership crisis at HDFC Bank, India’s largest private lender, where a single resignation letter triggered a ₹1 lakh crore ($12 billion) wipeout in market value.

1. The Banking Ecosystem: A Power Map

In high finance, power is not a simple ladder but a web of competing mandates. We categorize these into four primary “Power Centers” that serve as the guardians of the institution. These roles are intentionally designed with natural “checks and balances” to ensure that the drive for quarterly performance does not bypass the guardrails of ethics.

The Guardians of the Institution

| Role | Core Mandate | Primary Concern |

| The Chairman | Ethical Oversight & Governance | Long-term institutional integrity and adherence to values. |

| Managing Director & CEO | Operational Execution & Growth | Quarterly performance, market share, and aggressive execution. |

| Board of Directors | Deliberative Refereeing | Succession planning and protecting shareholder interests. |

| The Regulator (RBI) | Systemic Stability | Preventing “contagion” that could threaten the national economy. |

While these roles appear distinct on paper, human dynamics and the “haze of crisis” can quickly blur the lines of authority. As we shall see, when the referee and the engine disagree, the entire system faces a “governance scare.”

2. The Chairman: The Moral and Strategic Compass

The Part-time or Non-executive Chairman—typically a seasoned administrator like Atanu Chakraborty, a retired 1985-batch IAS officer—serves as the bank’s ethical braking system. Unlike the CEO, the Chairman does not manage daily loan disbursements. Instead, he ensures the bank’s “practices” align with its stated “values.”

The Responsibilities of the Chairman:

- Moral Oversight: Acting as the final arbiter on whether corporate behaviors meet the “integrity test.”

- Board Leadership: Setting the agenda for strategic shifts, such as the $10 billion merger between HDFC and HDFC Bank.

- Regulatory Liaison: Ensuring the bank’s internal culture satisfies the stringent requirements of the central bank.

In the HDFC crisis, Chairman Chakraborty used the most potent tool in a non-executive’s arsenal: the resignation letter. By citing a conflict of “ethics,” he signaled to the market that the bank’s moral compass was spinning:

“Certain happenings and practices within the bank, that I have observed over the last two years, are not in congruence with my personal values and ethics.”

This shift in the Chairman’s oversight focus from strategy to ethics was the primary catalyst for the subsequent market panic.

3. The CEO: The Operational Engine and Growth Driver

If the Chairman is the compass, the Managing Director (MD) & CEO is the engine. At HDFC, Sashidhar Jagdishan embodies this role—the professional “insider” tasked with aggressive expansion and operational stability.

Critical CEO Responsibilities and Survival Benefits:

- Driving Growth: Managing the massive expansion of branches and digital upgrades. Benefit: Maintains market dominance and offsets high cost-to-income ratios.

- Managing Integration: Overseeing the post-merger synergy of the HDFC Ltd. transition. Benefit: Realizes approximately $10 billion in synergies to stabilize the bank’s high Loan-to-Deposit Ratio (LDR).

- Accountability Fixation: Directly intervening in operational scandals, such as the termination of three senior executives (Sampath Kumar, Harsh Gupta, and Payal Mandhyan) following the mis-selling of Credit Suisse AT1 bonds at the Dubai DIFC branch. Benefit: Protects the bank from further regulatory bans from bodies like the Dubai Financial Services Authority (DFSA).

The Friction of Term Renewal A CEO’s authority is fundamentally tied to their “term renewal.” The HDFC crisis peaked when it was revealed that Chairman Chakraborty insisted on a “thorough performance review” before approving Jagdishan’s third term. When a Chairman demands rigorous oversight and the Board appears “baffled” by these demands, it creates a “governance overhang.” Investors perceive this not as a routine review, but as a lack of confidence in the captain of the ship.

4. The Board of Directors: The Deliberative Referee

The Board of Directors is a collective body of oversight, yet its power is concentrated in the Nomination and Remuneration Committee (NRC). This committee is the ultimate referee, deciding who earns what and who keeps their job.

Persuasion Tactics vs. Actionable Outcomes

| Board’s Persuasion Tactics | Actionable Outcomes |

| Asking the Chairman to “reconsider” or “take back some of the language” in his letter. | Appointing Keki Mistry (ex-HDFC CEO) as Interim Chairman same-day with RBI approval. |

| Seeking specifics on “ethical concerns” when the Chairman remained “not forthcoming.” | Briefing the RBI at 7 PM to ensure no “regulatory contagion” occurred. |

| Attempting to frame the exit as a “personal relationship issue” rather than a systemic failure. | Directing the NRC to meet within a month to finalize the CEO’s term extension or succession. |

The Role of an Interim Chairman The appointment of Keki Mistry (age 71) was a calculated move in “Institutional Signaling.” By choosing a veteran insider who was the architect of the bank’s parent company, the Board signaled “systems over personality.” Mistry’s role was to provide a psychological floor, assuring the market that the bank’s “governance is top class” despite the interpersonal friction.

5. The Regulator (RBI): The Ultimate Arbiter of Stability

For a “Systemically Important Bank,” the Reserve Bank of India (RBI) is the final backstop. The regulator’s role is to ensure that a boardroom brawl does not turn into a national bank run.

Three Specific RBI Interventions in the HDFC Crisis:

- Affirming Governance: The RBI issued a rare public statement asserting there were “no material concerns” regarding conduct or governance.

- Approving Interim Leadership: Providing same-day approval for Keki Mistry’s interim chairmanship to prevent a leadership vacuum.

- Monitoring Conduct: Engaging in “intense and cohesive engagement” with management on the way forward regarding international compliance (Dubai operations).

The Power of “Refining the Narrative” The most potent tool of a regulator is its ability to define reality for the market. By stating that the bank was “well-capitalised” and its financial position “satisfactory,” the RBI provided the psychological floor that stopped the stock’s freefall.

6. Case Study Synthesis: The Anatomy of a Leadership Shake-up

Chronology of a Crisis (March 2026)

- [x] March 17: Chairman Atanu Chakraborty signs his resignation letter citing ethical “happenings and practices.”

- [x] March 18: The Board is informed during an NRC meeting; the bank files the cryptic resignation with exchanges late at night.

- [x] March 19: Market panic ensues. HDFC Bank shares hit a 52-week low (₹770), losing ₹1 lakh crore ($12B) in market value.

- [x] March 20: The RBI, the Government, and Interim Chairman Keki Mistry enter “firefighting mode” to stabilize the stock.

The “So What?” for the Learner: Why did a disagreement over a “performance review” cost $12 billion? Because markets hate ambiguity. When a Chairman resigns over “ethics” without providing specifics, investors do not assume a minor rift; they price in a “governance scare.” The loss was not due to bad loans, but to the perceived breakdown of the “checks and balances” between the Compass and the Engine.

| The Conflict | The Institutional Lesson |

| Chairman vs. CEO over a “thorough performance review” for term renewal. | Succession planning is a market-moving force; any hint of leadership discontinuity is viewed as a risk. |

| Vague resignation citing “values and ethics.” | Transparency is the currency of trust. Ambiguity in high-level exits creates a “governance overhang” that devalues the firm. |

| Mis-selling of Credit Suisse AT1 bonds in Dubai branch. | International operations require rigorous domestic oversight; local failures can have global reputational consequences. |

7. Glossary for the Aspiring Banker

- AT1 Bonds: High-risk “Additional Tier-1” contingent convertible bonds that were written off (rendered worthless) during the Credit Suisse collapse; HDFC faced internal scandal regarding their mis-selling in Dubai.

- Loan-to-Deposit Ratio (LDR): A financial metric (currently near 100% for HDFC) indicating how much of a bank’s deposits are being lent out; a high LDR signals potential liquidity and funding sustainability concerns.

- Nomination and Remuneration Committee (NRC): A critical Board-level committee responsible for overseeing the performance, appointment, and pay of the CEO and other senior directors.

- Systemically Important Bank: A bank so significant to the national economy that the regulator (RBI) provides extra oversight to ensure its failure does not cause systemic collapse.