1. Introduction: The Debt-Free Triumph and the Mirage of Volume

For the sophisticated investor, the headline of the decade for Chambal Fertilisers & Chemicals Ltd. appeared on March 31, 2025: the company became entirely debt-free for the first time in five years. This aggressive deleveraging marks the climax of a ten-year saga of fiscal volatility, spanning from the recovery efforts of 2016 to the high-stakes projections of 2026.

However, beneath this “clean slate” lies a complex narrative that challenges the most basic tenant of retail investing: that more sales equals more profit. Chambal serves as a premier case study in operational complexity, where record-breaking revenue often masks underlying fragility. This briefing dissects the counter-intuitive mechanics of Chambal’s financial history to reveal how efficiency, not just volume, dictates the true ceiling of a fertilizer giant.

2. The 2023 Revenue Mirage: A Masterclass in Deleveraging Necessity

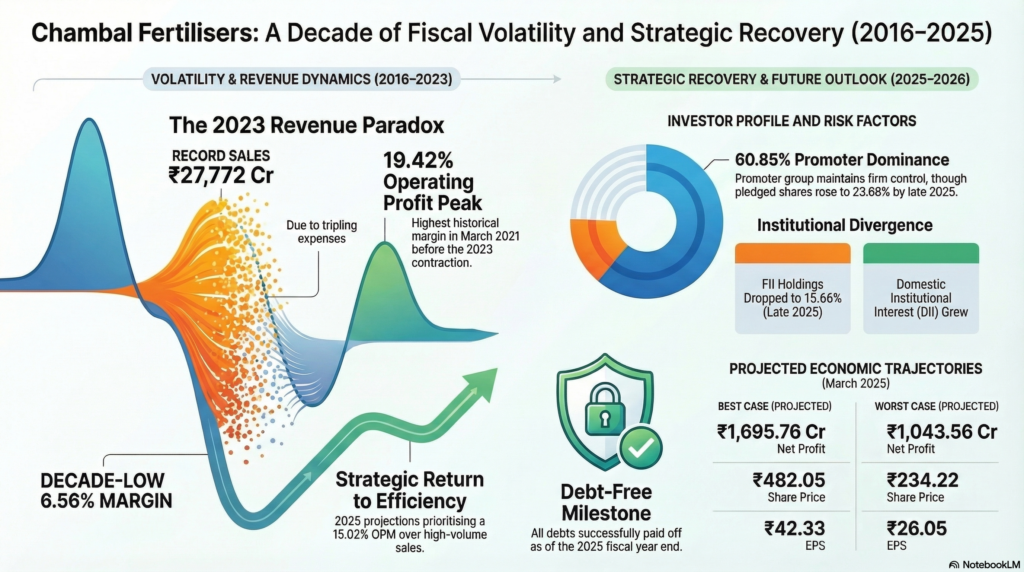

The fiscal year ending March 2023 stands as a cautionary monument in Chambal’s books. The company achieved its highest sales in history—reaching 27,772.81—yet net profit crashed to 1,034.22. This disconnect was not an accident; it was a systemic failure of cost management under the weight of external shocks.

The Profit Crash breakdown:

- Operational Expense Spikes: Costs exploded to 25,950.66, nearly tripling year-on-year and swallowing the revenue surge whole.

- The Interest Burden: Interest costs jumped to 320.02 (up from 108.88), a painful reminder of why the 2025 debt-free milestone became a strategic imperative.

- Margin Erosion: Operating Profit Margins (OPM) collapsed to a decade-low of 6.56%.

For the strategist, 2023 was the “never again” moment that forced the company to pivot from a volume-at-any-cost model to one focused on disciplined deleveraging and margin protection.

3. The Efficiency Mandate: Why OPM is the Critical Analytical Tool

In a sector governed by commodity prices and government subsidies, the Operating Profit Margin is the only metric that truly captures internal health. Chambal’s OPM history resembles a rollercoaster, reflecting the sheer difficulty of maintaining profitability in a shifting regulatory landscape.

Key Margin Milestones | Fiscal Year | Operating Profit Margin (OPM) | Strategic Context | | :— | :— | :— | | Mar-16 (The Start) | 7.26% | Early recovery phase | | Mar-21 (The Peak) | 19.42% | Peak operational efficiency | | Mar-23 (The Low) | 6.56% | The Revenue Mirage anomaly | | Mar-25 (Projected) | 15.02% | Post-deleveraging recovery |

The swing from nearly 20% to just 6.5% highlights the “Peak-to-Trough” risk that sophisticated investors must model. As the company moves toward 2026, the strategy has shifted definitively: management is now prioritizing a 15%+ OPM over raw revenue growth.

“These figures serve as a critical analytical tool for assessing long-term monetary stability and growth trends.” — Source Context

4. The Promoter Paradox: Leveraged Conviction or Red Flag?

As of December 2025, a tension emerged in the shareholding pattern. On one hand, the promoter group increased its pledging from 19.05% in March to 23.68% by the end of the year. In isolation, rising pledging is a red flag suggesting liquidity pressure.

However, a strategist must look at the “double-down” behavior observed in early 2026. Promoter entities like CM Airtime Promotion LLP and Ganges Securities were active open-market buyers in March 2026, steadily increasing their stakes. This suggests a “Promoter Paradox”: insiders are using pledged credit to increase their “skin in the game,” signaling a high-conviction bet on the recovery, even as they take on significant personal leverage.

5. The Institutional Tug-of-War: FII Anxiety vs. DII Confidence

The final quarter of 2025 saw a sharp 2.68% divestment by Foreign Institutional Investors (FIIs), whose holdings dropped to 15.66%. To understand this exit, we must link three disparate operational headwinds:

- The Gadepan-I Incident: An unscheduled stoppage at the Gadepan-I plant due to a “stripper leak” (a critical failure in the urea processing unit) eroded short-term EBITDA.

- The Subsidy Debt Trap: Stretched working capital saw subsidy debtors—monies owed by the government—jump sevenfold to a staggering ₹1,979 crores.

- The G-3 Expiry: Looming uncertainty over the Gadepan-III plant’s subsidy incentives (expiring Dec 2026) has made foreign capital nervous about “normalized returns.”

Conversely, Domestic Institutional Investors (DIIs) and mutual funds like Kotak and Groww Nifty Chemicals ETFs have been accumulators. The domestic thesis is focused on the Technical Ammonium Nitrate (TAN) plant. By diversifying into TAN—used in mining and explosives—Chambal is moving away from the volatile, government-dependent urea subsidy cycle toward a high-margin, industrial chemical future.

6. The Skew of Uncertainty: Analyzing the 2026 Risk-Reward

As we look toward the 2025/26 close, the market valuation reflects a significant “recovery premium.” The projected P/E ratio has jumped to 15.19 (from 10.74 in 2024), suggesting investors are already paying for the best-case scenario.

However, the “Gap of Uncertainty” reveals a dangerous downward skew for current entrants:

- Best-Case Price (482.05): Offers a modest ~12% upside from the current price of approx ₹428.55.

- Worst-Case Price (234.22): Represents a potential 45% collapse if the company fails to meet its optimal expense targets.

In this environment, valuation is not a product of sentiment, but a hostage to operational precision. If the company fails to manage its projected 17,870.56 expense ceiling, the market valuation could easily halve.

7. Conclusion: The Floor vs. The Ceiling

Chambal Fertilisers has successfully built a “floor” of stability by becoming debt-free and stabilizing its OPM at 15%. Yet, legacy ghosts remain. The recent ₹96.86 Lakh tax penalty for Assessment Year 2011-12—relating to contested deductions for anicut construction on the Parwan River—highlights the lingering regulatory friction inherent in large-scale infrastructure.

The road to 2026 presents a choice for the investor: Do you value the safety of a debt-free balance sheet and the “floor” of domestic cash flows, or are you wary of the “ceiling” of uncertainty created by plant leakages and subsidy expiries? In this sector, the most expensive mistake is assuming that a record-breaking top line is the same thing as a winning bottom line.